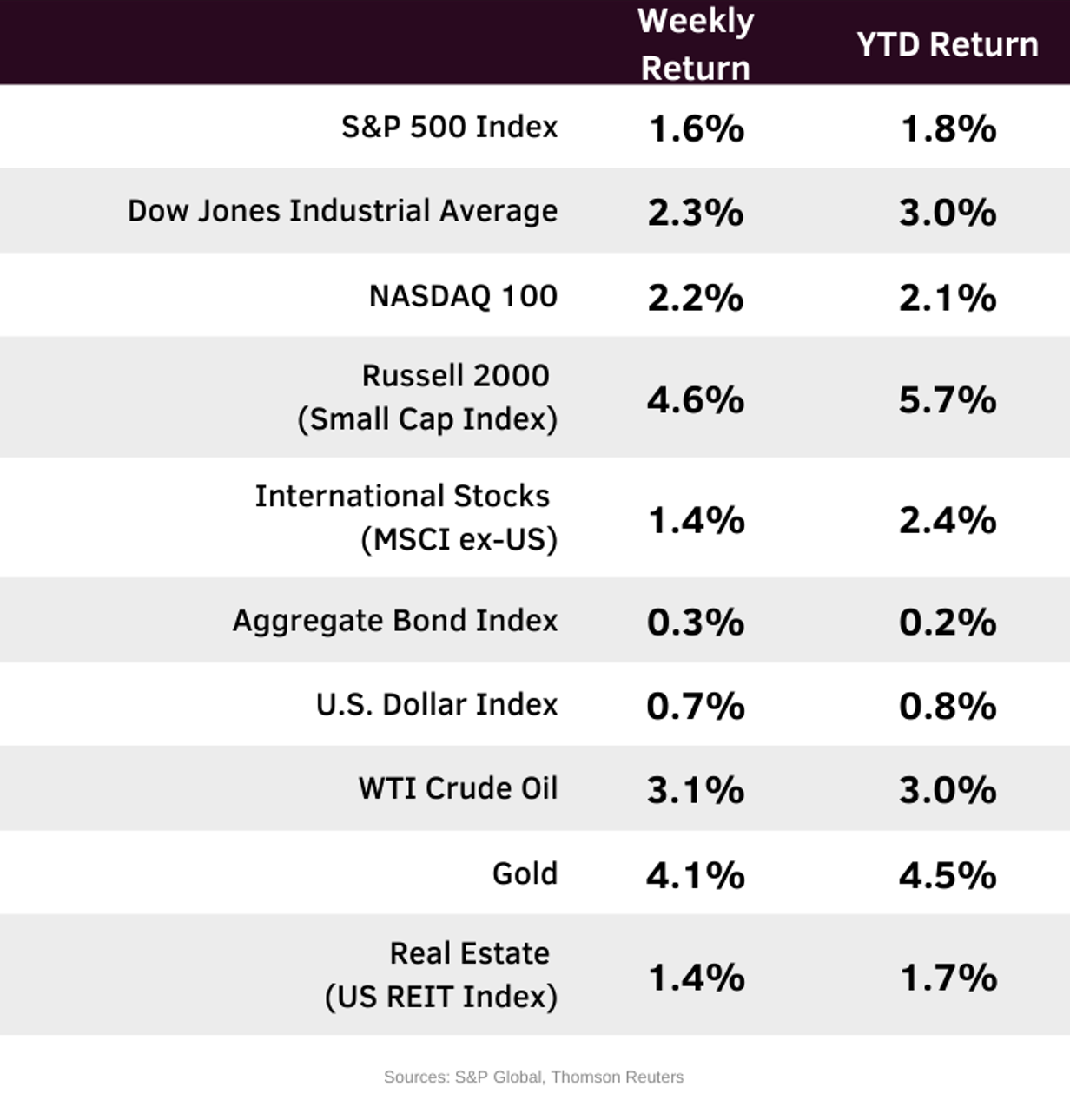

Stocks had a solid first full week of trading in the new year. For the week, the S&P 500 Index was +1.6%, the Dow Jones Industrials +2.3%, and the NASDAQ +2.2%. The Consumer Discretionary, Materials, and Industrial sectors led the S&P 500 Index for the week, while the Utility, Technology, and Real Estate sectors lagged. The 10-year U.S. Treasury note yield was 4.167% at Friday’s close versus 4.190% the previous week.

The labor market continues to see a headwind. The December Employment Situation report showed 50,000 net new jobs created versus an expectation of 73,000. November job growth was also revised down to 56,000 from previous report of 64,000. The December unemployment rate fell to 4.4% from 4.5% in November.

This week we will see reports on inflation with the December Consumer Price Index (CPI) scheduled for Tuesday and Producer Price Index (PPI) scheduled for Wednesday. Federal Reserve monetary policy for the first half of the year hinges on striking a balance between employment and inflation. For the first half of 2026, CME Fed funds futures have shifted to forecasting a single 0.25% reduction in the Fed funds rate at the June Federal Open Market Committee (FOMC) meeting.

The fourth quarter earnings reporting season begins this week with 14 companies in the S&P 500 Index scheduled to report earnings. Quarterly earnings are expected to grow by 8.3% with revenue growth of 7.7%. Full-year 2025 earnings are expected to grow by 12.4% with revenue growth of 7.0% and 2026 full-year earnings are expected to grow by 14.9% with revenue growth of 7.3%.

In our Dissecting Headlines section, we look at the outlook for fourth quarter earnings by sector.

Financial Market Update

Dissecting Headlines: Fourth Quarter Earnings

For the fourth quarter of 2025, S&P 500 earnings growth is currently forecast at +8.3%. Data from FactSet shows eight of the eleven sectors are forecast to show year-over-year earnings growth. The Technology sector is expected to have the highest year-over-year growth at +25.9%, followed by the Materials sector at +9.0%, and the Financial sector at +8.3%. Rounding out the growing sectors are Communication Services at +6.1%, Utilities at +4.7%, Real Estate at +2.4%, Consumer Staples at +0.7%, and Health Care at +0.2%. The three sectors expected to show a decline in year-over-year earnings are the Industrial sector at -0.5%, Energy at -1.7%, and Consumer Discretionary at -3.5%.

Fourth quarter revenue growth for the S&P 500 is currently forecast at +7.7%. The highest revenue growth is expected in the Technology sector at +18.0%, followed by Communication Services at +10.2%, and Health Care at +9.1%. Ten of eleven sectors are forecast to show year-over-year revenue growth. The other seven revenue growth sectors are Financials at +8.0%, Real Estate at +6.3%, Industrials at +5.8%, Consumer Staples at +5.3%, Utilities at +4.6%, Consumer Discretionary at +4.5%, and Materials at +3.0%. The only sector expected to show a decline in year-over-year revenue is the Energy sector at -2.2%.

The actual earnings results for companies and sectors relative to these expectations, along with their future outlooks, are key determinants of price performance. Major themes for the reporting period include capital spending and implementation of AI, hiring and work force reduction trends, the impact of tariffs and trade, and the health of the consumer.