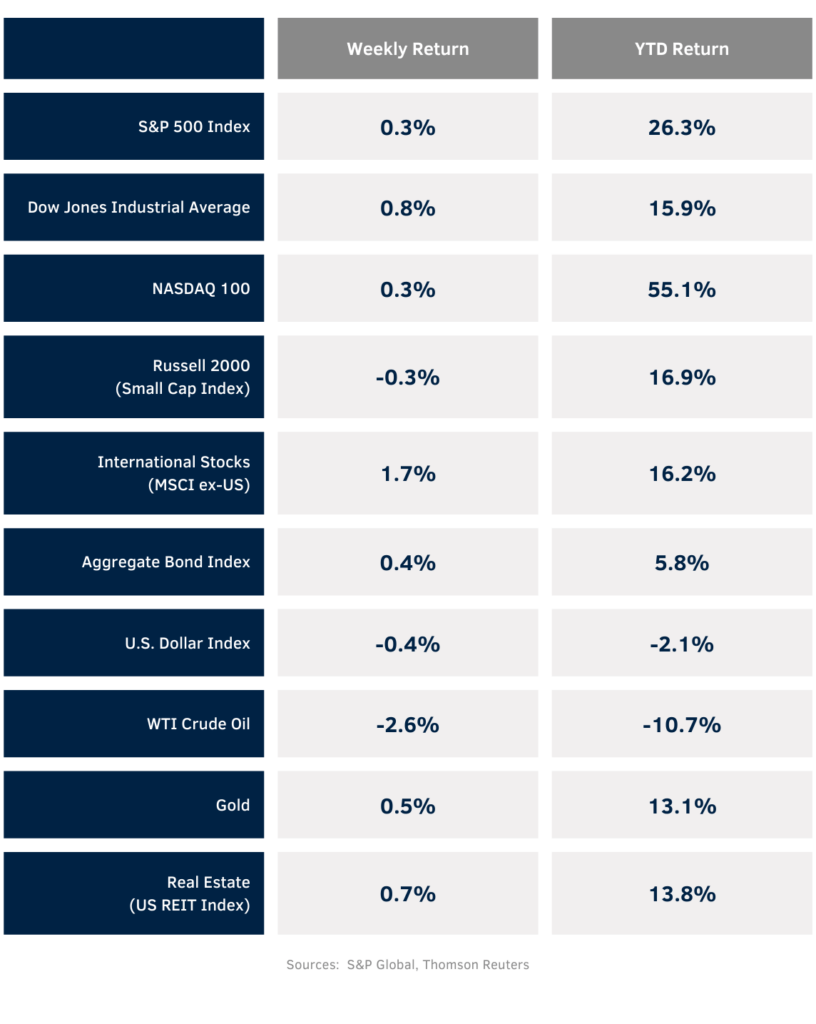

The equity markets had a quiet, but positive, last week of the year. The weekly return for the S&P 500 Index was +0.3%, the Dow was +0.8%, and the NASDAQ was +0.3%. The S&P 500 Index was led by the Utility, Consumer Staples, and Real Estate sectors. The Energy, Consumer Discretionary, and Communication Services sectors lagged. The 10-year U.S. Treasury note yield decreased to 3.860% at Friday’s close versus 3.908% the previous week.

The first major economic data point of the year is scheduled for Friday with the release of the December Employment Situation Report. A continued softening in job growth is likely needed to keep the Fed on track for an eventual easing of monetary policy. The current CME Fed funds futures show a 0.25% decrease in the Fed funds rate as early as March.

Fourth quarter earnings reports begin at the end of next week. Current fourth quarter expectations for the S&P 500 Index are earnings growth of 5.2% and revenue growth of 2.6%. For full-year 2023, S&P 500 Index earnings are expected to grow by 3.1% with revenue growth of 1.9%. For full-year 2024, earnings are expected to grow by 11.1% with revenue growth of 5.1%.

In our Dissecting Headlines section, we look at investor sentiment heading into 2024.

Financial Market Update

Dissecting Headlines: Investor Sentiment

We start 2024 with above average Bullish sentiment and below average Bearish sentiment in the American Association of Individual Investors (AAII) Sentiment Survey. The week of December 27th survey had Bullish sentiment of 46.3% versus the historical average of 37.5% and Bearish sentiment of 25.1% versus the historical average of 31.0%.

The survey is often seen as a contrarian indicator since below-average market returns have often followed unusually high levels of optimism while above-average market returns have often followed unusually low levels of optimism. While not a perfectly correlated indicator, we can see the value in being greedy when others are fearful and fearful when others are greedy.

The contrarian value of the survey can be illustrated from just a few months ago when the November 1, 2023 survey was at a 1-year Bearish high of 50.3% right before the two-month rally took off to close out 2023. Additionally, if we go back a year ago, the December 29, 2022 survey was 26.5% Bullish and 47.6% Bearish before 2023’s large return. The survey was more in-line with historical averages before 2022’s big down year with December 30, 2021 Bullish sentiment at 37.7% and Bearish sentiment at 30.1%.