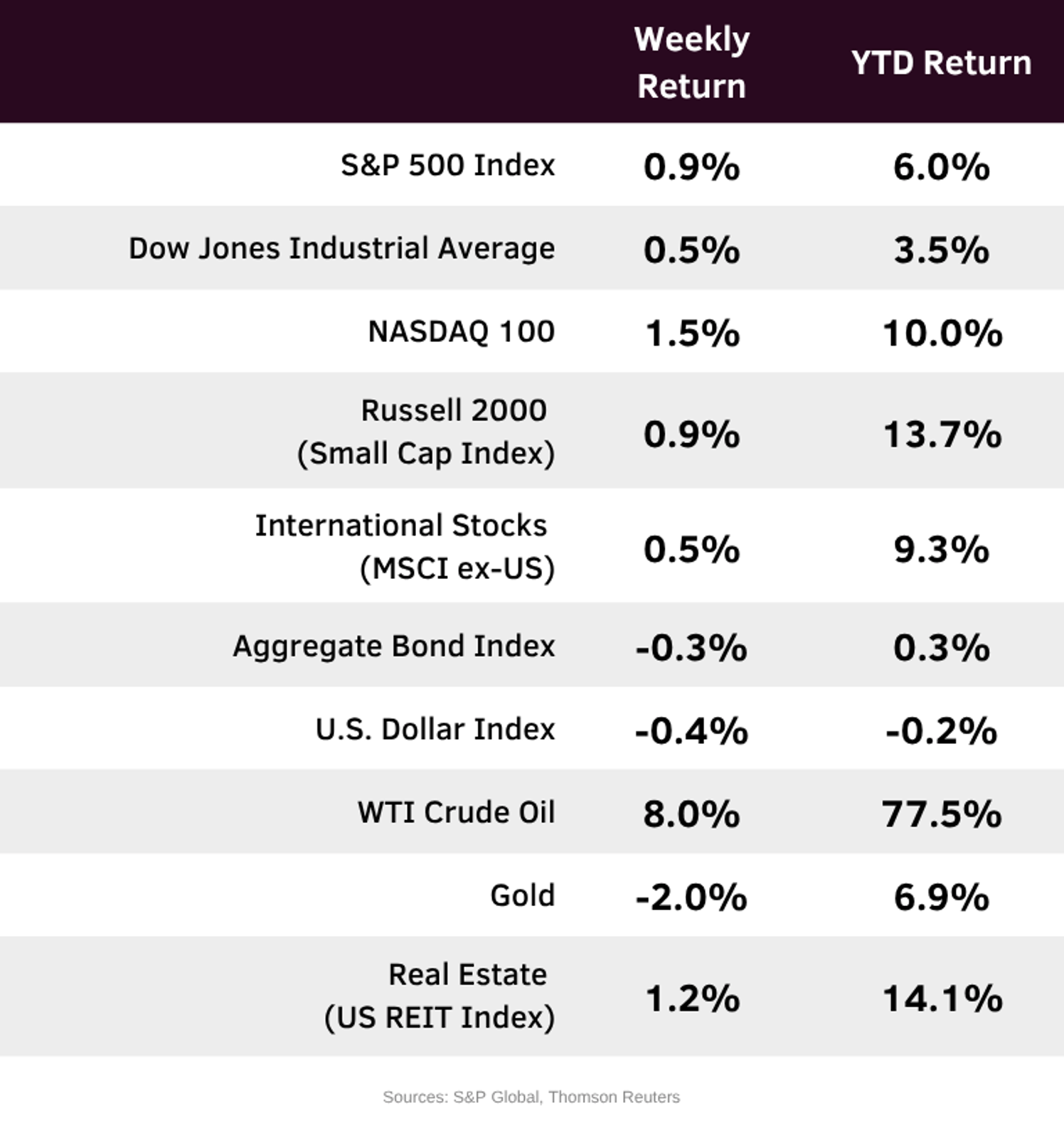

Strength in quarterly earnings reports pushed stocks higher. For the week, the S&P 500 Index was +0.9%, the Dow Jones Industrials +0.5%, and the NASDAQ +1.5%. The Communication Services, Energy, and Consumer Staples sectors led the S&P 500 Index for the week, while the Materials, Technology, and Industrial sectors lagged. The 10-year U.S. Treasury note yield was 4.383% at Friday’s close versus 4.303% the previous week.

The Federal Reserve held short-term interest rates steady at its April policy meeting. Fed Chair nominee Kevin Warsh has passed the Senate Banking Committee and is set for a full Senate confirmation vote next week. This would put him in position to preside over the next Federal Open Market Committee (FOMC) meeting in mid-June when the FOMC should publish its updated Summary of Economic Indicators to set its policy path for the second half of the year.

First quarter Gross Domestic Product (GDP) growth was 2.0% versus expectation for 2.1% and versus 0.5% last quarter. Business investment contributed to more than half the growth with the Information Processing Equipment category contributing 83 basis points of the overall 200 basis points of GDP growth. Exports were strong, but imports were stronger creating a negative impact on Net Exports.

With 64% of companies in the S&P 500 Index already reported, the quarterly earnings reporting period continues this week with another 126 companies scheduled to report results. First quarter earnings are expected to grow by 27.1% and quarterly revenue growth is expected at 11.1%. Full-year 2026 earnings are expected to grow by 20.6% with revenue growth of 9.7%. Earnings growth expectations have taken a large move up since the reporting period began in early April.

In our Dissecting Headlines section, we take another look at the year-to-date revisions in earnings growth for the S&P 500 Index.

Financial Market Update

Dissecting Headlines: Earnings Revisions

Last week, we wrote about how the shift in focus from geopolitical events to first quarter earnings results has been a strong contributing factor to the market recovery in April. Expectations for earnings growth took another step forward last week following earnings results from several Mega cap companies that raised both the expectation for first quarter growth and growth for the year.

With 63% of companies reported in the S&P 500 Index, the consensus estimate for the first quarter earnings growth has increased to 27.1% versus 15.1% the week prior and versus 13.0% at the end of March just prior to the reporting period beginning. Revenue growth for the first quarter has also increased to 11.1% versus 10.3% the week prior and 9.7% at the end of March.

Expectations for full-year 2026 earning have also taken another move up. The current expectation for S&P 500 Index earnings growth for 2026 is 20.6% versus 18.6% the week prior and 17.1% at the end of March. Revenue growth expectations for the year have also increased to 9.7% versus 9.5% the week prior and 8.6% at the end of March.

It reminds us of the Warren Buffet quotes that builds on Benjamin Graham’s work, “In the short run, the market is a voting machine…but in the long run, it is a weighing machine.”