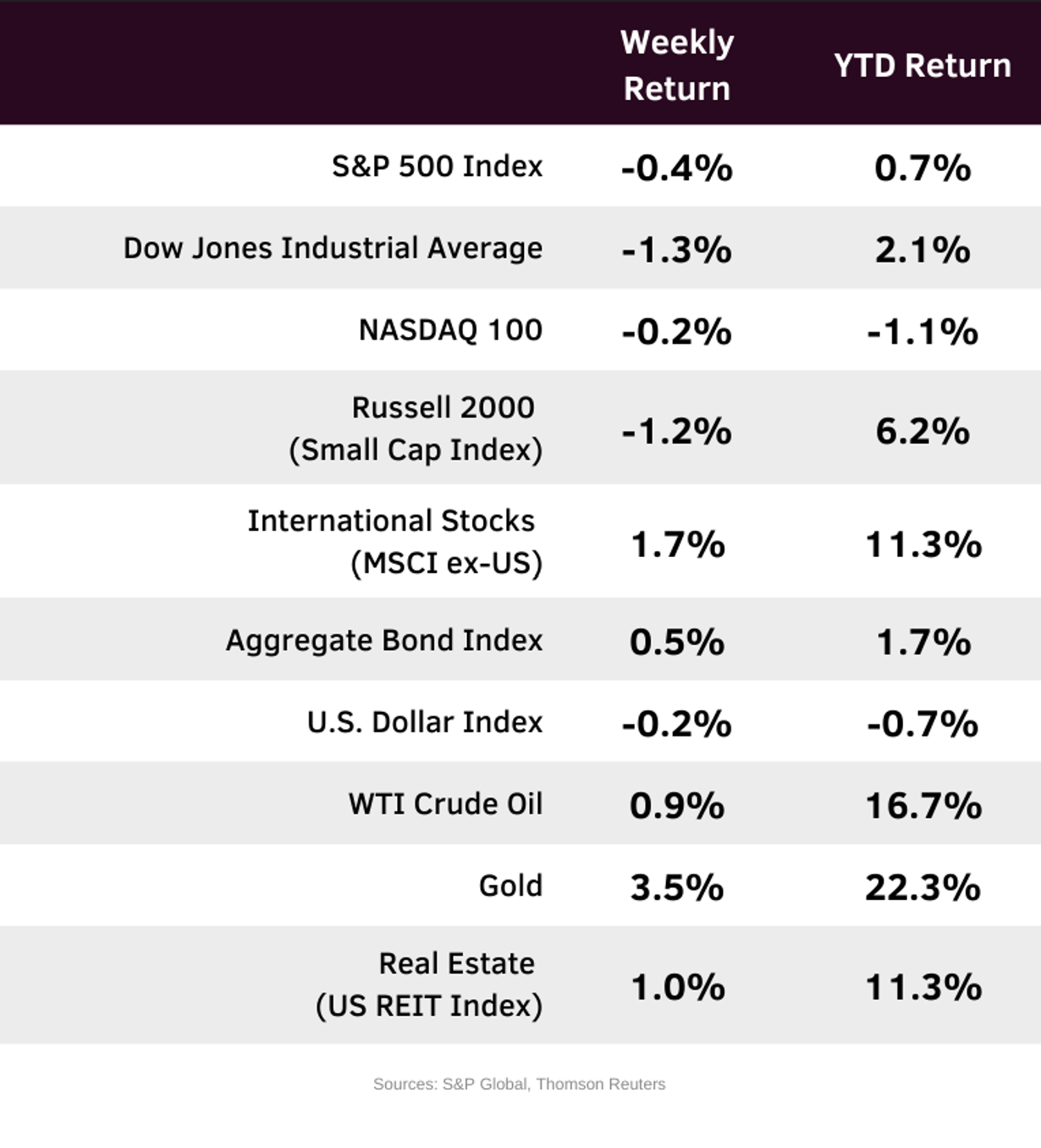

Equity markets closed out the week on a down note, driven by concerns over AI disruption, higher than expected wholesale inflation, and geopolitical tensions. For the week, the S&P 500 Index was -0.4%, the Dow Jones Industrials -1.3%, and the NASDAQ -0.2%. The Utility, Consumer Staples, and Health Care sectors led the S&P 500 Index for the week, while the Technology, Financial, and Consumer Discretionary sectors lagged. The 10-year U.S. Treasury note yield was 3.962% at Friday’s close versus 4.082% the previous week.

January wholesale prices, measured by the Producer Price Index (PPI), showed sticky inflation, specifically in services versus goods. The January PPI was +0.5% month-over-month versus an expectation of +0.3%. Inflation in services was +0.8% month-over-month and inflation in goods was -0.3% month-over-month. This week the February Employment Situation report is scheduled for Friday. CME Fed funds futures currently indicate 0.25% reductions in short-term interest rates at the July and October Federal Reserve policy meetings.

Over the weekend, the U.S. and Israel initiated military action against Iran after talks to curb Iran’s nuclear program fell through. This is likely to keep investors on edge over coming days as the action is on-going.

This week 10 companies in the S&P 500 Index are scheduled to report earnings. With 96% of companies already reported, the fourth quarter earnings are expected to grow by 14.2% and quarterly revenue growth is expected at 9.4% Full-year 2025 earnings are expected to grow by 13.6% with revenue growth of 7.7% and 2026 full-year earnings are expected to grow by 14.7% with revenue growth of 7.7%.

In our Dissecting Headlines section, we look at the current conflict in Iran.

Financial Market Update

Dissecting Headlines: Iran Conflict

The U.S. and Iran did not come to any agreements on limiting Iran’s nuclear program in Geneva last week. The U.S. and Israel started a military campaign over the weekend that has so far eliminated most of Iran’s top tier leadership. Iran’s retaliation has spread to other countries in the region, possibly bringing them into the conflict.

Oil prices are currently higher as Iran is the 9th largest oil producer in the world and has the 4th highest proved reserves. Additionally, Iran’s geographic position near the Strait of Hormuz is limiting seaborne transit of oil and LNG out of the Persian Gulf area. Some current reports cite traffic down 70%.

Depending on the duration of the conflict and safety concerns in the Gulf, there could be days to weeks of disruption. We are seeing a typical pattern of investors shunning risk, as equities look to trade down in the near-term and money flows into traditional safe havens such as gold and government bonds.

Most of Iran’s oil was going to China, at below market prices. Like recent events in Venezuela, the events in Iran could shift some of the global oil supply dynamics. In the interim, several OPEC+ countries, to include Saudi Arabia, plan to raise oil production by 1.65 million barrels per day starting in April. U.S. officials are not currently planning to release oil from the strategic petroleum reserve.

The duration and extent of disruptions and their economic impact should play out over the coming days and weeks.